Strategy builder taking ages to build new strategies

5 replies

Julianrob

6 years ago #117762

Hi,

a couple of days ago I downloaded the strategy builder trial to see how it worked. I’m quite interested and prepared to buy it. I’ve selected some basic but detailed amount of parameters to run strategies on the EURUSD 1HR chart and set to random generation.

Among the ranking options settings I have set to filter out

PF: < 1.3,

PF (OOS) < 1.3,

Return D/D ratio < 3.0

Return DD (OOS) < 2.0

% wins 50%

% wins (OOS) 50%

Number of trades < 300

Number of trades (OOS) < 80

Now are my parameters too limited? If so, please can someone guide me

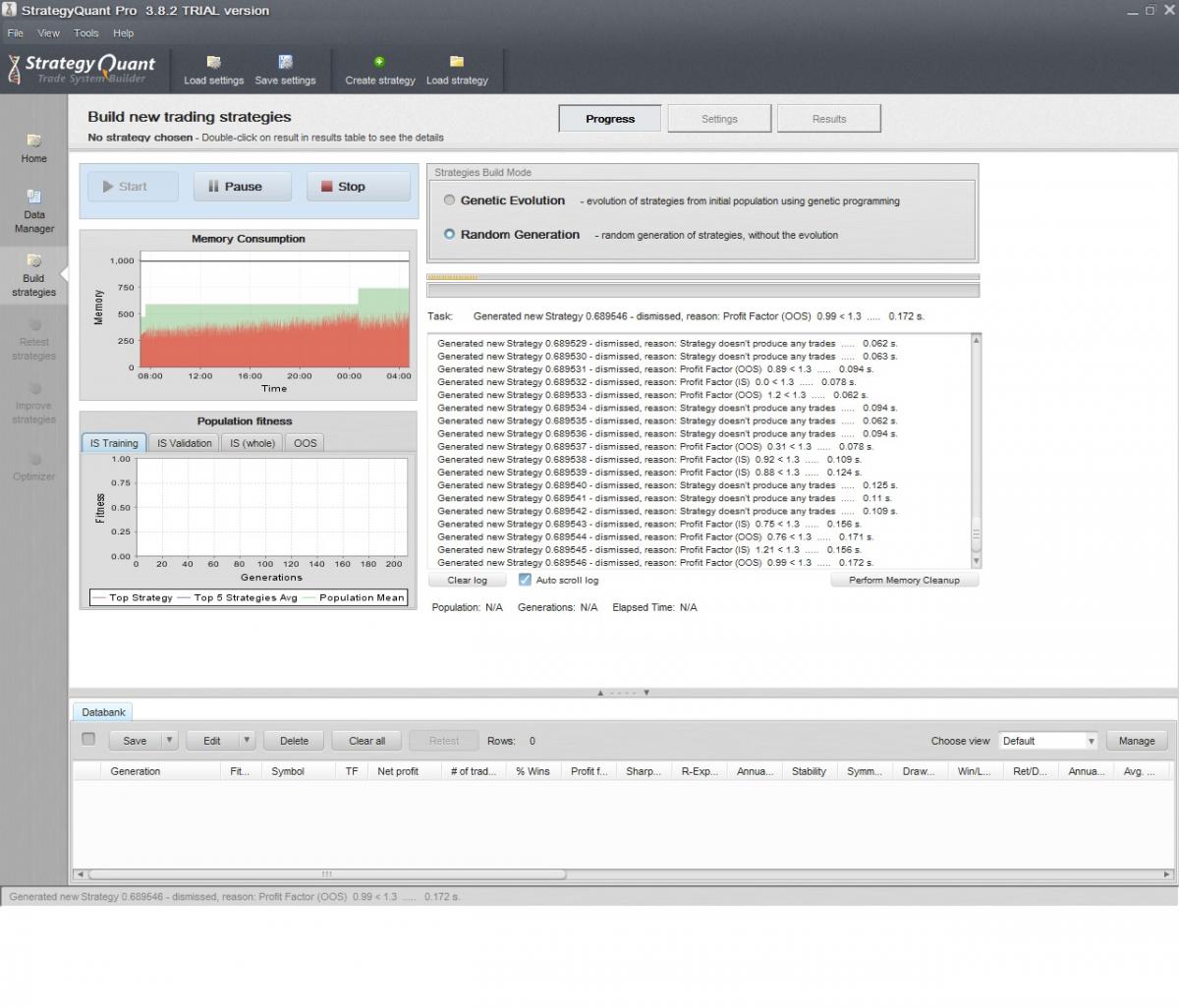

So far the system builder has been scanning for literally ages (Around 20 hours) and is up to 0.694000 strategy. It has not yet yielded any strategies. I’m just wondering how long a typical scan should take because this seems to be taking a very very long time? Please refer to attached image.

Regards, Julian

SQ-Builder.jpg

SQ-Builder.jpgtomas262

6 years ago #144731

Hello,

it does not seems that much strict to me. How much historical data you used to develop strategies on? How many years? What building blocks / order types you used? You can try to temporarily lighten up the dismiss conditions to see effects

hankeys

6 years ago #144746

use genetic evolution and reduce %win to 30%

You want to be a profitable algotrader? We started using StrateQuant software in early 2014. For now we have a very big knowhow for building EAs for every possible types of markets. We share this knowhow, apps, tools and also all final strategies with real traders. If you want to join us, fill in the FORM.

Karish

6 years ago #144750

Julianrob

6 years ago #144765

Ok, thanks for your advice, I’ll try that out.

I’ve loosened my parameters and managed to get some strategies listed! Now, I am running robustness checks on these strategies on different timeframes and another currency, as the tutorial recommends. I have come up with something that looks very profitable, nice equity curve which actually gets better during out of sample time. The strategy looks really good.

This brings me to another Q: Does the SQ strategy builder build these robots on a test rig using tick-by-tick data or open of bars?

When I download the best strategy that’s passed all the robust checks, I load it into MT4. When I backtest it on exactly the same asset, T/F, spread and time range, on both open bar and tick-by-tick, I get entirely different results. The strategy is actually losing money, and the equity line is all over the place, not like the SQ builder equity line. Tick by tick results is 90% modelling accuracy on MT4 backtest.

Am I missing something, and how to get 99% accuracy?

Thanks again in advance for your help. Julian

Karish

6 years ago #144772

Reread the SQ’s pdf guide and use tickstory or even better tickdatasuite.

Viewing 5 replies - 1 through 5 (of 5 total)