Release of SQX 139 Dev 1 and what’s planned for year 2024

We’d like to announce the release of the new SX 139 Dev 1 version – note that this is a development version for testing, not the final 139 version. Most …

Přejít k obsahu | Přejít k hlavnímu menu | Přejít k vyhledávání

Portfolio Master is a new Quant Analyzer feature that allows you build optimal portfolio.

Let’s say you have 20 different strategies, but your account size allows you to trade only 5 of them.

So you have to choose which 5 of these 20 strategies to trade – in other words how to build an optimal portofolio of 5 strategies that will have the best possible profit with minimal worst case drawdown.

Another example from diversified futures world – you have a good trading system that works on a broad range of markets and a capital of $ 50k. Let’s say there are 20 markets available for trading.

We know $ 50k is not enough money to trade twenty markets, but it could be possible to trade 5 or 6 markets with this account.

The question is how to optimally choose these five or six markets from the list of twenty.

With diversification in mind, we should pick markets from different sectors – currency, stock index, interest rate, energy, grain, meat, softs, etc.

But which market from every sector should we pick to get the best results?

Why to use Portfolio Master?

The only way to find the best portfolio is to examine every combination of strategies/markets and choose the portfolio that produces the best Return / Drawdown ratio.

This is exactly what Portfolio Master does for you.

If you wonder how many possible combinations have to be tested, it can be computed using the formula: N! / (N – P)! * P!

where N is total nuber of strategies we can use and P is the size of our desired portfolio.

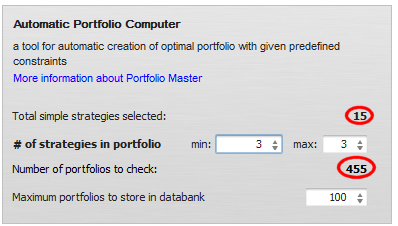

For N = 15 (15 systems available) and P = 5 (portfolio of 5 systems) there are 3003 possible combinations!

This is just too many to be tested manually.

You can locate Portfolio Master icon on the left panel.

The first step is to load and select simple strategies that we want to combine into portfolio.

You can load your strategies in a standard way and then select the ones to use in Simple strategies databank.

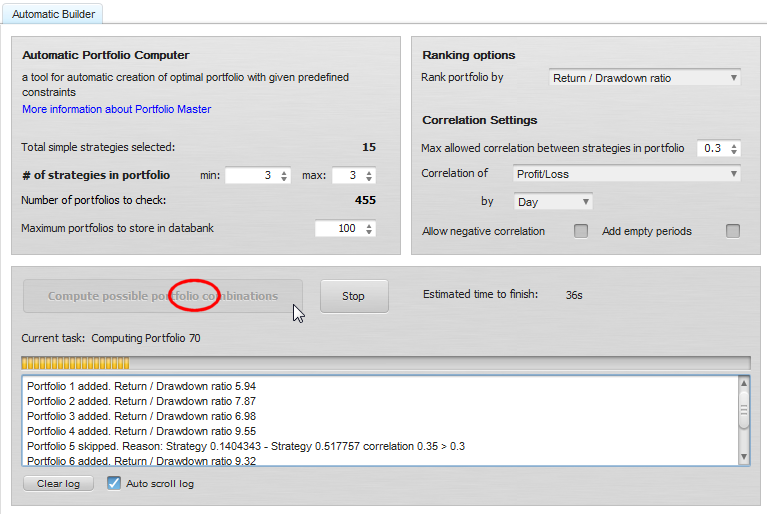

Automatic Builder tells you the number of strategies selected and also the total combinations that have to be tested.

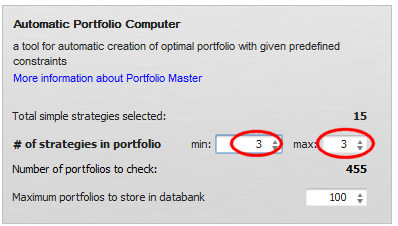

The configuration is simple – the main thing you need to do is to configure how many strategies should your portfolio consist of. You can choose a range, for example from 5 to 7 strategies.

Note that changing this number will also change the number of portfolios to check.

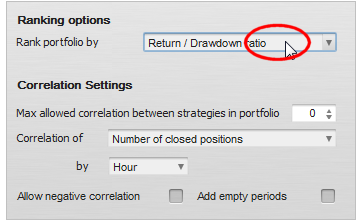

Ranking function is a function that computes the “fitness” of the created portfolio. Fitness value determines how the portfolios will be ranked against each other and which of the portfolios will be selected as “top” in Portfolios databank.

Ranking can be based on just simple Net Profit of portfolio, or it can be more complex and use for example return / Drawdown ratio.

The important thing is that ranking functions are customizable, you can create your own ranking function in Snippets.

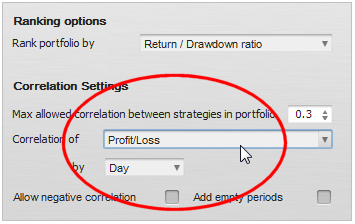

One of the last things that can be controlled in created portfolios is correlation – you can specify that you don’t want portfolio whose strategies are too correlated.

The correlation can be based on Profit/Loss or open or close trades or positions, by hour, day, week or month and again, it is customizable using Snippets.

By limiting sectors you can configure how many strategies per sector / market are allowed for each strategy. We explain how to use the sectors in additional article.

Press Compute button to start with portfolios evaluation. As the program works the top X portfolios ar estored into Portfolio databank. If databank is full and new better portfolio is found, it will replace the worst one from the databank.

You can stop this process anytime or wait until it cancels.

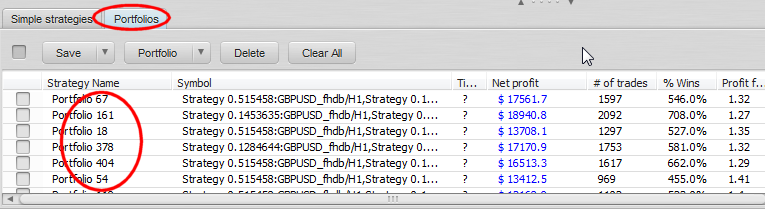

Finish: Evaluating the results

Your Portfolio databank now contains the top generated portfolios selected using your ranking function. You can browse them and look at them more closely in the Analyzer.

Please note that the number of possible combinations grows very quickly with the number of simple strategies used and size of portfolio.

For example, for N = 100 (100 systems available) and P = 20 (portfolio of 20 systems) there are 535 983 370 403 809 682 970 possible combinations!

Even with the speed of Quant Analyzer it is not possible to compute them all.

The only thing we can do is to choose more reasonable inputs.

We’d like to announce the release of the new SX 139 Dev 1 version – note that this is a development version for testing, not the final 139 version. Most …

Dive into Algorithmic Trading Without the Coding Headache! Are you intrigued by algorithmic trading but dread the thought of coding? Today marks the beginning of our exciting series that’s about …

Tomas Vanek

Tomas Vanek5. 3. 2024

In this interview, we catch up with Naoufel, a seasoned trader, to explore his journey through the stormy market of 2023. Naoufel is successful trader with verfied track record who …

Ellie Souckova

Ellie Souckova12. 12. 2023

How to get merged source code with Portfolio master ?

Currently, result source code has comment that ‘// Pseudo Source Code of Portfolio [11.18.33.46.53.138.165.183]’ on header section.

But, body code seems single strategy.